Secrets of Mental Math, Arthur Benjamin [management books to read .txt] 📗

- Author: Arthur Benjamin

Book online «Secrets of Mental Math, Arthur Benjamin [management books to read .txt] 📗». Author Arthur Benjamin

To determine a 15% tip, we have a few options. If you have mastered the techniques of Chapter 2, and are comfortable with multiplying by 15 = 5 × 3, you can simply multiply the bill by 15, then divide by 100. For example, with a $42 bill, we have 42 × 15 = 42 × 5 × 3 = 210 × 3 = 630, which when divided by 100, gives us a tip of $6.30. Another method is to take the average of a 10% tip and a 20% tip. From our earlier calculation, this would be

Perhaps the most popular approach to taking a 15% tip is to take 10% of the bill, cut that amount in half (which would be a 5% tip), then add those two numbers together. So, for instance, with a $42 bill, you would add $4.20 plus half that amount, $2.10, to get

Let’s use all three methods to compute 15% on a bill that is $67. By the direct method, 67 × 3 × 5 = 201 × 5 = 1005, which when divided by 100 gives us $10.05. By the averaging method, we average the 10% tip of $6.70 with the 20% tip of $13.40, to get

Using the last method, we add $6.70 to half that amount, $3.35 to get

$6.70 + $3.35 = $10.05

Finally, to calculate a 25% tip, we offer two methods. Either multiply the amount by 25, then divide by 100, or divide the amount by 4 (perhaps by cutting the amount in half twice). For example, with a $42 bill, you can compute 42 × 25 = 42 × 5 × 5 = 210 × 5 = 1050, which when divided by 100 produces a tip of $10.50. Or you can divide the original amount directly by 4, or cut in half twice: half of $42 is $21, and half of that is $10.50. With a $67 bill, I would probably divide by 4 directly: since 67 = 4 = 16¾, we get a 25% tip of $16.75.

NOT-TOO-TAXING CALCULATIONS

In this section, I will show you my method for mentally estimating sales tax. For some tax rates, like 5% or 6% or 10%, the calculation is straightforward. For example, to calculate 6% tax, just multiply by 6, then divide by 100. For instance, if the sale came to $58, then 58 × 6 = 348, which when divided by 100 gives the exact sales tax of $3.48. (So your total amount would be $61.48.)

But how would you calculate a sales tax of 6½% on $58? I will show you several ways to do this calculation, and you choose the one that seems easiest for you. Perhaps the easiest way to add half of a percent to any dollar amount is to simply cut the dollar amount in half, then turn it into cents. For example, with $58, since half of 58 is 29, simply add 29 cents to the 6% tax (already computed as $3.48) to get a sales tax of $3.77.

Another way to calculate the answer (or a good mental estimate) is to take the 6% tax, divide it by 12, then add those two numbers. For example, since 6% of $58 is $3.48, and 12 goes into 348 almost 30 times, then add 30 cents for an estimate of $3.78, which is only off by a penny. If you would rather divide by 10 instead of 12, go ahead and do it. You will be calculating 6.6% instead of 6.5% (since = 0.6) but that should still be a very good estimate. Here, you would take $3.48 and add 34¢ to get $3.82.

Let’s try some other sales tax percentages. How can we calculate 7¼% sales tax on $124? Begin by computing 7% of 124. From the methods shown in Chapter 2, you know that 124 × 7 = 868, so 7% of 124 is $8.68. To add a quarter percent, you can divide the original dollar amount by 4 (or cut it in half, twice) and turn the dollars into cents. Here, 124 = 4 = 31, so add 310 to $8.68 to get an exact sales tax of $8.99.

Another way to arrive at 31¢ is to take your 7% sales tax, $8.68, and divide it by 28. The reason this works is because = ¼ For a quick mental estimate, I would probably divide $8.68 by 30, to get about 29¢, for an approximate total sales tax of $8.97.

When you divide by 30, then you are actually computing a tax of %, which is approximately 7.23% instead of 7.25%.

How would you calculate a sales tax of 7.75%? Probably for most approximations, it is sufficient to just say that it is a little less than 8% sales tax. But to get a better approximation, here are some suggestions. As you saw in the last example, if you can easily calculate a ¼% adjustment, then simply triple that amount for the ¾% adjustment. For example, to calculate 7.75% of $124, you first calculate 7% to obtain $8.68. If you calculated that ¼% is 31¢, then ¾% would be 93¢, for a grand total of $8.68 + 0.93 = $9.61. For a quick approximation, you can exploit the fact that = .777 is approximately .75, so you can divide the 7% sales tax by 9 to get slightly more than the .75% adjustment. In this example, since $8.68 divided by 9 is about 96¢, simply add $8.68 + 0.96 = $9.64 for a slight overestimate.

We can use this approximation procedure for any sales tax. For a general formula, to estimate the sales tax of $A.B%, first multiply the amount of the sale by A%. Then divide this amount by the number D, where A/D is equal to 0.B. (Thus D is equal to A times the reciprocal of B.) Adding these numbers together gives you the total sales tax (or an approximate one, if you rounded D to an easier nearby number). For instance, with 7.75%, the magic divisor D would be  , which we rounded down to 9. For sales tax of

, which we rounded down to 9. For sales tax of  %, first compute the sales tax on 6%, then divide that number by 16, since

%, first compute the sales tax on 6%, then divide that number by 16, since  . (To divide a number by 16, divide the number by 4 twice, or divide the number by 8, then by 2.) Try to come up with methods for finding the sales tax in the state that you live in. You will find that the problem is not as taxing as it seems!

. (To divide a number by 16, divide the number by 4 twice, or divide the number by 8, then by 2.) Try to come up with methods for finding the sales tax in the state that you live in. You will find that the problem is not as taxing as it seems!

SOME “INTEREST-ING” CALCULATIONS

Finally, we’ll briefly mention some practical problems pertaining to interest, from the standpoint of watching your investments grow, and paying off money that you owe.

We begin with the famous Rule of 70, which tells you approximately how long it takes your money to double: To find the number of years that it will take for your money to double, divide the number 70 by the rate of interest.

Suppose that you find an investment that promises to pay you 5% interest per year. Since 70 ÷ 5 = 14, then it will take about 14 years for your money to double. For example, if you invested $1000 in a savings account that paid that interest, then after 14 years, it will have $1000(1.05)14 = $1979.93. With an interest rate of 7%, the Rule of 70 indicates that it will take about 10 years for your money to double. Indeed, if you invest $1000 at that annual interest rate, you will have after ten years $1000(1.07)10 = $1967.15. At a rate of 2%, the Rule of 70 says that it should take about 35 years to double, as shown below:

$1000(1.02)35 = $1999.88

A similar method is called the Rule of 110, which indicates how long it takes for your money to triple. For example, at 5% interest, since 110 ÷ 5 = 22, it should take about 22 years to turn $1000 into $3000. This is verified by the calculation $1000(1.05)22 = $2925.26. The Rule of 70 and the Rule of 110 are based on properties of the number e = 2.71828 … and “natural logarithms” (studied in precalculus), but fortunately we do not need to utilize this higher mathematics to apply the rules.

Now suppose that you borrow money, and you have to pay the money back. For example, suppose that you borrow $360,000 at an annual interest rate of 6% per year (which we shall interpret to mean that interest will accumulate at a rate of 0.5% per month) and suppose that you have thirty years to pay off the loan. About how much will you need to pay each month? First of all, you will need to pay $360,000 times 0.5% = $1,800 each month just to cover what you owe in interest. (Although, actually, what you owe in interest will go down gradually over time.) Since you will make 30 × 12 = 360 monthly payments, then paying an extra $1,000 each month would cover the rest of the loan, so an upper bound on your monthly payment is $1,800 + $1,000 = $2,800. But fortunately you do not need to pay that much extra. Here is my rule of thumb for estimating your monthly payment.

Let i be your monthly interest rate. (This is your annual interest rate divided by 12.) Then to pay back a loan of $P in ? months, your monthly payment M is about

In our last example, ? = $360,000, and i = 0.005, so our formula indicates that our monthly payment should be about

Notice that the first two numbers in the numerator multiply to $1,800. Using a calculator (for a change) to compute (1.005)360 = 6.02, we have that your monthly payment should be about $1,800(6.02)/5.02, which is about $2,160 per month.

Here’s one more example. Suppose you wish to pay for a car, and after your down payment, you owe $18,000 to be paid off in five years, with an annual interest rate of 4%. If there was no interest, you would have to pay $18,000/60 = $300 per month. Since the first year’s interest is $18,000(.04) = $720, you know that you will need to pay no more than $300 + $60 = $360. Using our formula, since the monthly interest rate is i = .04/12 = 0.00333, we have and since (1.00333)60 = 1.22, we have a monthly payment of about $60(1.22)/(0.22) = $333.

We conclude with some exercises that we hope will hold your interest.

GUESSTIMATION EXERCISES

Go through the following exercises for guesstimation math; then check your answers and computations at the back of the book.

Round these numbers up or down and see how close you come to the exact answer:

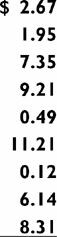

Mentally estimate the total for the following column of prices by rounding to the nearest 50¢:

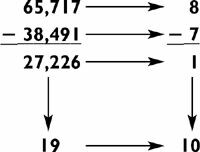

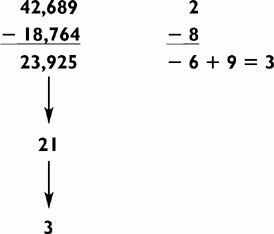

Estimate the following subtraction problems by rounding to the second or third digit:

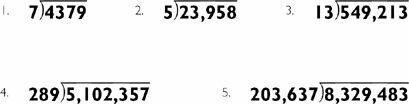

Adjust the numbers in a way that allows you to guesstimate the following division problems:

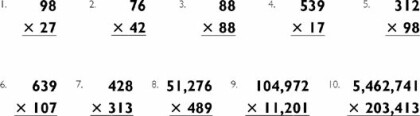

Adjust the numbers in a way that allows you to guesstimate the following multiplication problems:

Estimate the square roots of the following numbers using the divide and average method:

1. Compute 15% of $88.

2. Compute 15% of $53.

3. Compute 25% of $74.

4. How long does it take an annual interest rate of 10% to double your money?

5. How long does it take an annual interest rate of 6% to double your money?

6. How long does it take an annual interest rate of 7% to triple your money?

7. How long does it take an annual interest rate of 7% to quadruple your money?

8. Estimate the monthly payment to repay a loan of $100,000 at an interest rate of 9% over a ten-year period.

9.

Comments (0)